In this comprehensive article, we delve into the world of loans and credit lines, exploring the fundamental dissimilarities between the two and analyzing the advantages and disadvantages they offer. If you are considering borrowing money for any purpose, it’s essential to grasp the distinctions between these financial tools to make an informed decision. So, let’s explore the Loan vs. Credit Line debate in detail.

A loan is a specific amount of money granted to a borrower based on their needs, intended for one-time use. Unlike credit lines, loans are not revolving, meaning the borrower cannot repeatedly access the credit once it’s repaid.

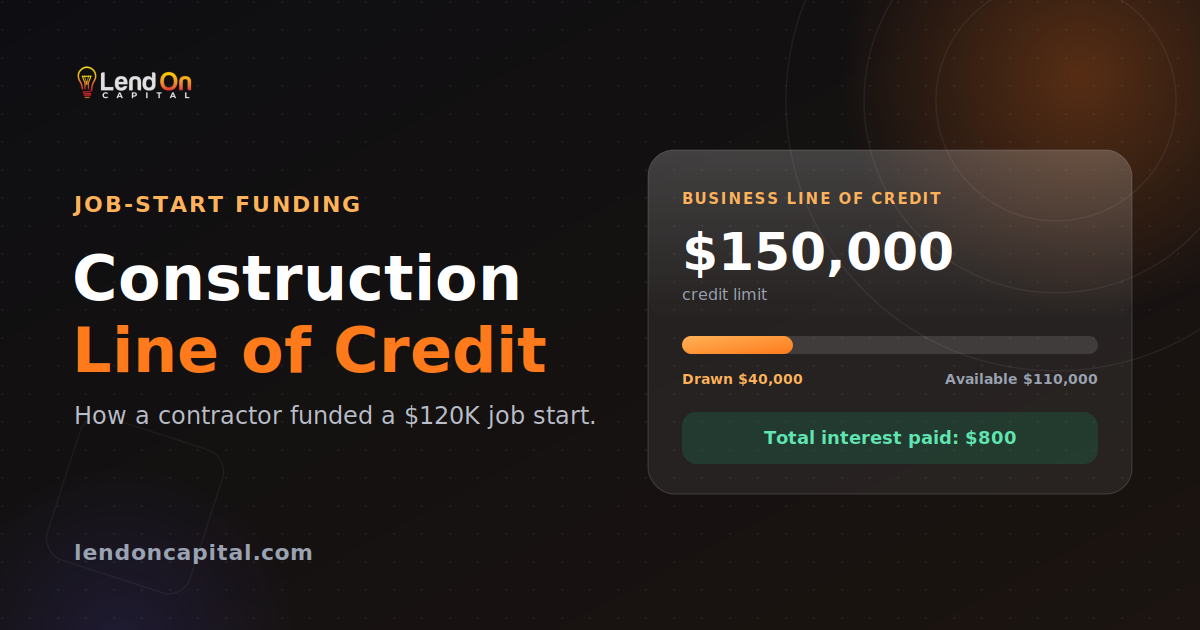

A business line of credit, represents the amount of money a borrower can repeatedly access from a bank or financial institution, similar to a credit card. It is a revolving credit, providing flexibility to use the funds for various purposes, such as everyday purchases, small renovations, or debt consolidation.

The borrower can withdraw funds from the credit line whenever needed, as long as the credit is available. The payment schedule can be weekly or monthly and comprises both interest and principal.

In conclusion, both business loans and business lines of credit have their advantages and are valuable financial tools for business owners. A business loan offers a lump sum amount with fixed interest rates for specific purposes, while a business line of credit provides flexibility for multiple borrowings and repayments within the credit limit. Consider your business’s specific needs, financial circumstances, and the purpose for which you need the funds when choosing between the two options.